Os autores também reúnem respostas para a eterna questão do juro real neutro alto para o Brasil:

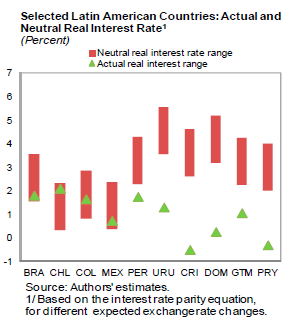

While the Brazilian neutral real interest rate (NRIR) has declined considerably over time, it still remains high by international standards. Various hypotheses have been formulated for this high neutral real interest rate level:

- Fiscal considerations. Brazilian public debt, at around 65 percent of GDP in gross terms, is high by regional standards. Moreover, there is a strong endogeneity between the level of the policy rate—the SELIC—and the level of public debt, given that about half of the domestic public debt is indexed to the SELIC. This restricts the degrees of freedom for monetary policy and feeds back into a higher than otherwise SELIC, and thus NRIR (World Bank, 2006). Similarly, Rogoff (2005) argues that Brazil incurs a significant default risk premium due to its inflationary history; an argument reinforced empirically by World Bank (2006).

- Low domestic savings. Brazil’s low domestic savings, and thus investment, is also cited as a reason for a higher NRIR (Fraga, 2005; Miranda and Muinhos; 2003; Hausmann, 2008; and Segura, 2012). However, Segura (2012) finds that low domestic savings cannot adequately explain the cross-country discrepancy.

- Institutional factors. Weak creditor rights and contractual enforcement have been cited as possible explanations for a higher NRIR (Arida et al., 2004; Rogoff, 2005). Lack of full central bank independence is also used to explain the high NRIR, though Nahon and Meuer (2009) find no changes in central bank’s credibility due to recent changes in its Board of Directors.

- Widespread financial indexation. There is strong inertia due to the indexation of financial contracts to the overnight interest rate (World Bank, 2006). While this indexation has maintained financial intermediation in Reais, it has created a system of unusually short duration financial contracts. The legacy of indexation to the overnight interest rate has created institutional and psychological inertia, and a path-dependency that has been difficult to dislodge. It has also made inflation less responsive to interest rate changes.

- Other Brazil-specific factors. Subsidized lending has resulted in credit market segmentation, pushing up market-determined interest rates. Other factors that might keep the nominal neutral interest rate high include an inflation target that is higher than in other emerging market economies and the minimum remuneration requirements in saving accounts (see Segura (2012) and Central Bank of Brazil (2012) for details).

Interessante ver que vários dos fatores listados vêm mudando (caindo parcela de dívida indexada a Selic, tentativas de reduzir a indexação, fim do piso para os juros da poupança, aumento dos prazos dos contratos, etc).

O trabalho também fala do efeito das chamadas medidas macroprudenciais na política monetária, mas não vou me alongar mais - se você se interessa pelo assunto, vale ir direto na fonte.

7 comentários:

excelente.

pergunta: o pib potencial em ~4%

por que ?

"número mágico" ?

É estimado por um modelo, como esses juros neutros...

Hoje o Tombini falou que é por aí. Eu chutaria menos, mas não muito, o que não faz grande diferença.

com relaçaõ ao PIB potencial, vc chegou a ver isso aqui ?

maovisivel.blogspot.com.br/2012/10/workin-man-blues.html

o AS começa a duvidar desse pib potencial na cada dos 4~4.5%.

achei interessante o ponto dele.

any thougths ?

Eu sempre achei que era mais baixo - na verdade acho que só o Mantega acha que é mais perto de 5%

http://drunkeynesian.blogspot.com.br/2012/04/alguns-fatos-subversivos-sobre.html

Brasil cresceu perto de 4% nos anos de boom de commodities, sem isso deve ser algo entre 3% e 3,5% - a esperança é que de fato esteja-se começando a investir em infraestrutura, educação, etc... Daqui a uns 10 anos sobe, se der certo.

é verdade, ótima discussão aquela.

abs

2 dúvidas:

- quais medidas existem para tentar reduzir a indexação?

- estamos começando a investir em infraestrutura e educação (nos comments) ???

Abs

Postar um comentário